Every account, every payment date. The dividend tracker built for FIRE investors who care about income — not price chaos.

Type a ticker. We fill in the name, current price, dividend rate, frequency, and next ex-dividend date automatically.

Most trackers obsess over price. Lensfolio obsesses over the income that actually funds your freedom.

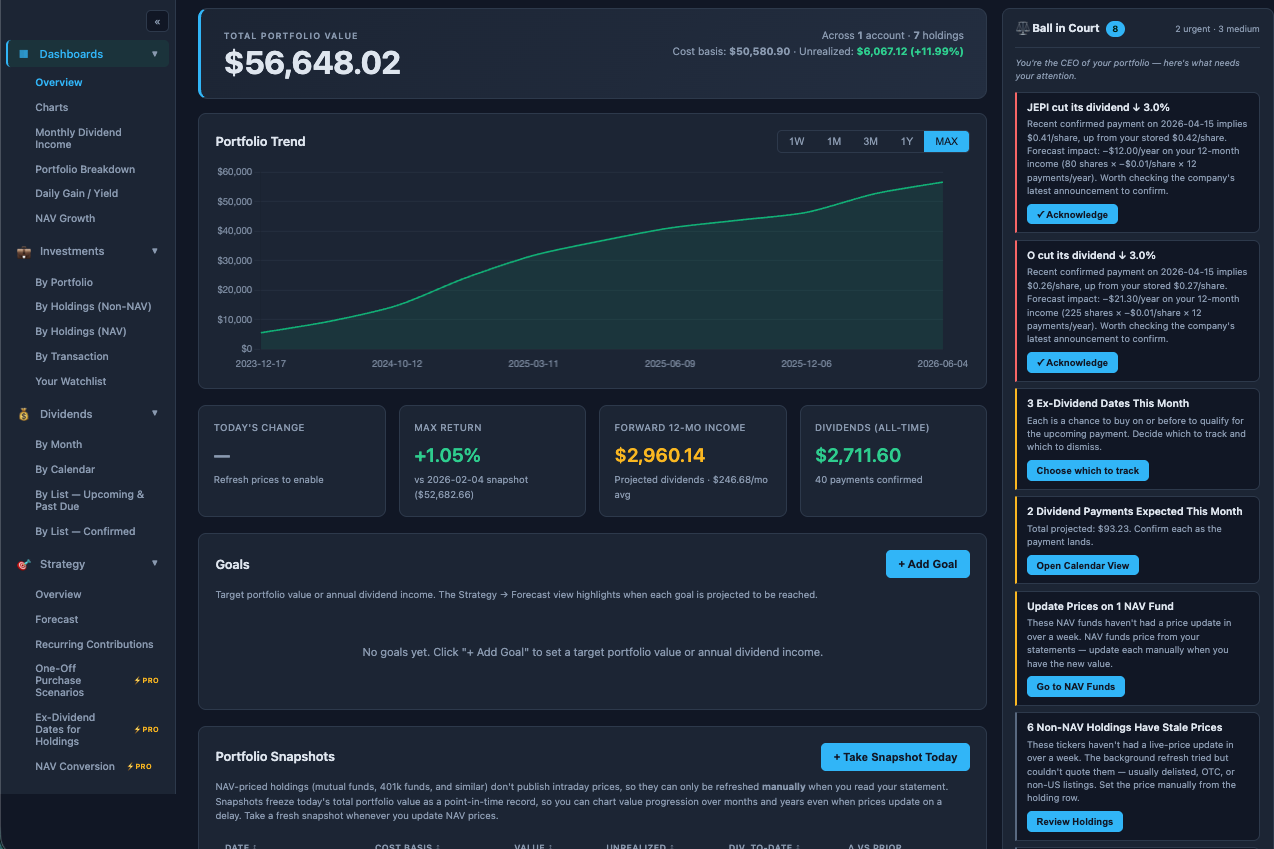

Project exactly what your portfolio will pay you over the next year — with DRIP compounding modeled per holding, per account. See the snowball roll forward in real numbers, not vague percentages.

Hold the same stock in Roth, Traditional, and Taxable. Reinvest in tax-advantaged accounts, take cash in taxable. Lensfolio is the only tracker built around the way real DGI investors actually structure positions.

Real 401(k) match structures aren't simple. Model tiered matches with per-period caps, annual caps, and YTD-already-received. Forecast how your full contribution stack — yours plus your employer's — accelerates your timeline.

Most trackers only handle assets with a public ticker. If your 401(k) holds an institutional-class fund — "SP 500 INDEX PL CL D," a target-date series, a stable-value fund — Lensfolio tracks its growth from your statements. Manual updates, full history, real compounding alongside the rest of your portfolio.

No spreadsheets. No CSV wrestling. No connecting your broker.

Type a ticker and the number of shares you own. Lensfolio fills in the price, frequency, and next ex-dividend date automatically.

Roth, Traditional, Taxable — and whether to reinvest dividends or take cash. You can change it per holding, per account.

Lensfolio shows your forward 12-month income, every upcoming payment, and how DRIP compounds your shares quarter after quarter.

Model recurring contributions, tiered 401(k) match, and one-off purchases on top of DRIP. The Strategy Forecast compounds it all together so you see — in dollars, not percentages — when each FIRE goal lands.

Everything you need under the hood — done quietly, done right.

Every upcoming ex-div and pay date in one view, with confirmation tracking.

Built for funds that auto-reinvest dividends inside the fund — target-date funds, 401(k) institutional shares, and most mutual funds — where investors only see a changing NAV.

Sign in anywhere. Phone, laptop, tablet — same data, encrypted in transit and at rest.

HTTPS everywhere. Database storage encrypted by Supabase. Passwords are hashed — we never see them.

We make money from subscriptions, not from you. Zero third-party trackers, zero advertising cookies.

You enter what you want to track — manually or via bulk import. Lensfolio never connects to your broker.

Founder · Dividend investor · Tired of spreadsheets

I'm a FIRE-pursuing dividend investor and I'd been running my portfolio in a tangled Google Sheet for years. The problem wasn't that the math was hard — it was that the math kept breaking every time a stock hiked its dividend, every time DRIP added new shares, every time I added an account.

Lensfolio is the tool I wished existed. It's intentionally narrow: it's for people building toward financial independence on dividend income, and it focuses on the specific things that crowd cares about. If that's you, I'd love your feedback. Email me directly at hello@lens-folio.com — I read every message.

Free works for most people. Pro is for serious dividend stacks that have outgrown a spreadsheet.

Everything you need to get started.

No credit card, no expiring trial

For the FIRE crowd running real dividend portfolios.

Save $29/year with annual billing

BETA50 at checkout for 50% off Pro for life — $4.50/mo or $39.50/yr, locked in as long as you stay subscribed. Limited to the first 100 beta sign-ups.| Feature | Free | Pro |

|---|---|---|

| Portfolios (Taxable, IRA, 401k, etc.) | 1 | Unlimited |

| Dividend stock / ETF holdings | Max 10 | Unlimited |

| Mutual fund (NAV) holdings | Max 1 | Unlimited |

| FIRE goals | Max 1 | Unlimited |

| Dividend calendar — every ex-div + pay date | ✓ | ✓ |

| Monthly dividend income view | ✓ | ✓ |

| Cloud sync across devices | ✓ | ✓ |

| 12-month DRIP-aware income forecast | ✓ | ✓ |

| FIRE drawdown modeling | ✕ | ✓ |

| One-off purchase scenarios | ✕ | ✓ |

| Ex-dividend dates planner | ✕ | ✓ |

| NAV-to-per-share conversion | ✕ | ✓ |

| Dividend coverage scenarios | ✕ | ✓ |

| CSV import for bulk transactions | ✕ | ✓ |

| Tax-lot tracking DRIP reinvestments auto-recorded from transactions — no manual lot entry |

✕ | ✓ |

| Multi-account DRIP control (per-portfolio) | ✕ | ✓ |

| Tiered employer match modeling | ✕ | ✓ |

| Priority email support · feature votes | ✕ | ✓ |

Stuck on the fence? Start free, upgrade the minute you hit a cap — your data carries over, no re-entry.

Sign up free and have a forecast running in five minutes. Pro is one click away when you outgrow the free tier.

Most portfolio trackers were built for one question: "What is my account worth right now?" That's the wrong question for dividend investors. The right question is: "What is this account going to pay me over the next 12 months — and how does that compound?"

If you've ever tried to answer that in a spreadsheet, you know the pain. You have to model ex-dividend dates per holding, frequency, DRIP shares purchased at varying prices, employer match across multiple accounts, and the tax-advantaged structure that determines whether each dollar gets reinvested or banked. Then your stocks announce a dividend hike, and the whole sheet drifts out of sync.

Lensfolio treats forward income as the primary metric, not a footnote. Every screen — dashboard, calendar, strategy, snapshots — orients around when payments arrive and how much. Add a holding and you immediately see: "This adds $X to your forward 12-month income." Hike your contribution and you see how the compound curve bends.

That reframing matters because dividend investing is a long game. Price will swing 30% in a bad year. Your dividend stream usually doesn't. A tracker that highlights price chaos and buries income is fighting your strategy, not supporting it.

Most trackers — even the paid ones — show you a flat projection: "You earned $X in dividends this year, so next year will be $X." That's wrong on two fronts. It ignores DRIP-purchased shares (which add to next year's payments) and ignores dividend rate changes (most quality dividend payers raise their distribution annually).

Lensfolio compounds DRIP at the per-payment level. When SCHD pays you $200 in March and you reinvest at $28.50, those new 7 shares are immediately included in your June calculation. Over a year, that's the difference between projecting $11,000 and actually receiving $11,847. Over a decade in your accumulation phase, it's the difference between hitting your FIRE number on schedule and missing it by 18 months.

The FIRE crowd that prefers dividend growth (DGI) over total-return indexing has a specific set of needs that mass-market tools ignore. They want to hold the same stock across multiple account types and apply different DRIP rules per account. They want tiered employer match modeling for their 401(k) — most matches aren't a flat 5%, they're "100% of first 3%, 50% of next 2%, capped annually." They want to see ex-dividend dates as a calendar, not a list. They want to model recurring contributions and watch the timeline shorten visibly. And they want all of it private and free of advertising.

Lensfolio is built for that exact stack. Start on the free tier, upgrade to Pro the moment you outgrow it, and use code BETA50 at checkout for 50% off Pro for life — yours as long as you stay subscribed.